Archive for February, 2009

ssh-keygen -t rsa

Then use this command to push the key to the remote server, modifying it to match your server name.

cat ~/.ssh/id_rsa.pub | ssh user@hostname 'cat >> .ssh/authorized_keys'

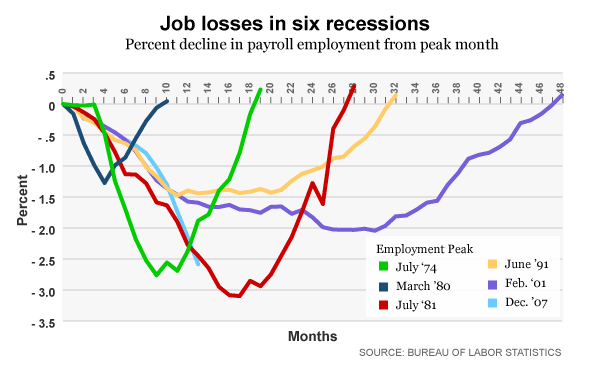

What is the responsibility of the government in times of recession? What is meant by “stimulating the economy”?

US GDP (in the long run) = number of working people * productivity of each working person.

Thus there are three levers the government can pull today to increase GDP by 2025.

- Increase the number of people

- Increase our productivity

- Increase the number of people willing to work

The first would require increased immigration or a higher birth rate. The second is a function of education and the capital stock (which the government is in the habit of depleting) and the third (in the case of full employment) is a matter of personal choice.

Over the long run, there is very little the government can do to increase per capita GDP other than ensuring optimal productivity of the workforce and creating conditions which would ensure full (or close to full) employment without inflation. Sacrificing productivity is always the long term peril as labor is shifted to the public sector.

On the demand side of the equation, the government has the option of preventing people from saving and enforcing spending. Of course, in the longer run, the only option is preventing people from spending or saving and allowing the government to do the spending for them. Consumption is merely shifted from the private sector to the public sector with no net increase in demand on the generous assumption that government spending is as efficient as private spending.

Hayek gave a convincing critique of government action’s ability to stimulate “aggregate demand.” Hayek viewed the boom and bust of the business cycle as primarily a monetary phenomenon created by governments’ artificial inflation of money and credit.

Sound money policy, conversely, allowed the disparate knowledge of millions of economic actors to be conveyed through the price system, rationally allocating capital and labor through relative prices. The problem with government attempts to manipulate the economy through fiscal policy — spending that takes resources away from those who are productive and redistributes it to politically favored interests — is that it is audacious. It assumes that government knows better how to spend and invest than individuals acting in their families’ best interest.

“The real question,” according to Hayek, “is not whether man is, or ought to be, guided by selfish motives but whether we can allow him to be guided in his actions by those immediate consequences which we can know and care for or whether he ought to be made to do what seems appropriate to somebody else who is supposed to possess a fuller comprehension of the significance of these actions to society as a whole.”

The usual retort to this argument is a variant on “in the long run we are all dead”. In the short run, then, the role of the government is to act as a counter-cyclical economic agent. Short runs turn easily into long runs, though, and short-lived is the president who decides the economy needs not “stimulating” but … what? We don’t even have a word for it.

David Brooks expressed this thought succinctly, if somewhat belatedly, with his call for “epistemological modesty”

redirect_to :action => ‘list’ forces the clients browser to request the list action.

render :action => ‘list’ will render the template list.rhtml without calling or redirecting to the list action.

Apparently “playing by the rules” , according to Obama, includes taking an adjustable mortgage that results in monthly payments equal to 43% (or more) of income. According to the Homeowner Affordability and Stability Plan

“For a sample household with payments adding up to 43 percent of his monthly income, the lender would first be responsible for bringing down interest rates so that the borrower’s monthly mortgage payment is no more than 38% of his or her income. Next the initiative would match further reductions in interest payments dollar-for-dollar with the lender to bring that ratio down to 31 percent…â€

So in the case of two families with identical earnings and living in identical houses we take the tax money of the responsible family that saved for a downpayment and give it to the irresponsible family that didn’t. And if you were responsible enough to rent until prices came down then you’re just out of luck.

Redistributing wealth based on income is a crude, but necessary, manner of levelling an uneven playing field. Redistribution based on debt introduces considerably more unfairness.

Panel discussion at Edge between behavioral economist, Kahneman and author Taleb on the economic crisis.

Note: They might be at the edge of thought but they certainly aren’t at the edge of the network! Get yourselves a CDN people!

I highly recommend Bort when you’re starting a new Ruby on Rails project. Assuming you’re using MySQL, the following steps are all that are necessary to get started:

- Download and unzip Bort into project folder

- Edit the database.yml and the settings.yml files

- Create the database: mysqladmin -u <username> -p create <db_name_development>

- If you’re using Dreamhost: add ‘host: mysql.<dbhostname>.com’ to your database.yml file (in the production environment)

- rake db:migrate

The following gems and plugins are the most popular as of Nov 12th, 2008:

- Javascript Framework: jQuery (56%), Prototype (43%)

- Skeleton: Bort

- Mocking: Mocha

- Exception Notification: Hoptoad

- Full text search: Thinking Sphinx

- Uploading: Paperclip

- User authentication: Restful_authentication (keep an eye on Authlogic)

- HTML/XML Parsing: Hpricot

- View Templates: Haml

NewRelic has a good article on the state of the Rails stack.

| Â | Â | BAC | GE | IBM | INTC | JNJ | KO | MCD | MMM | MRK | MSFT | PFE | PG | T | WMT | Return | StdDev |

| Bk Of America Cp | BAC | Â | Â | Â | Â | Â | Â | Â | Â | Â | Â | Â | Â | Â | Â | -95.8% | 9.8% |

| Gen Electric Co | GE | 0.63 | Â | Â | Â | Â | Â | Â | Â | Â | Â | Â | Â | Â | Â | -80.9% | 4.8% |

| Intl Business Mac | IBM | 0.66 | 0.68 | Â | Â | Â | Â | Â | Â | Â | Â | Â | Â | Â | Â | -48.1% | 3.0% |

| Intel Corporation | INTC | 0.57 | 0.64 | 0.74 | Â | Â | Â | Â | Â | Â | Â | Â | Â | Â | Â | -66.9% | 4.1% |

| Johnson And Johns | JNJ | 0.50 | 0.58 | 0.67 | 0.69 | Â | Â | Â | Â | Â | Â | Â | Â | Â | Â | -28.4% | 2.5% |

| Coca Cola Co The | KO | 0.39 | 0.45 | 0.56 | 0.66 | 0.72 | Â | Â | Â | Â | Â | Â | Â | Â | Â | -35.8% | 2.8% |

| Mcdonalds Cp | MCD | 0.54 | 0.62 | 0.66 | 0.66 | 0.69 | 0.66 | Â | Â | Â | Â | Â | Â | Â | Â | -5.5% | 2.7% |

| 3 M Company | MMM | 0.56 | 0.66 | 0.68 | 0.68 | 0.77 | 0.66 | 0.75 | Â | Â | Â | Â | Â | Â | Â | -39.3% | 3.0% |

| Merck Co Inc | MRK | 0.55 | 0.62 | 0.71 | 0.75 | 0.80 | 0.66 | 0.73 | 0.72 | Â | Â | Â | Â | Â | Â | -23.6% | 3.5% |

| Microsoft Corpora | MSFT | 0.58 | 0.55 | 0.75 | 0.80 | 0.72 | 0.68 | 0.68 | 0.68 | 0.73 | Â | Â | Â | Â | Â | -54.0% | 4.0% |

| Pfizer Inc | PFE | 0.61 | 0.60 | 0.66 | 0.70 | 0.76 | 0.64 | 0.67 | 0.71 | 0.80 | 0.70 | Â | Â | Â | Â | -37.5% | 3.2% |

| Procter Gamble | PG | 0.53 | 0.62 | 0.68 | 0.69 | 0.84 | 0.70 | 0.73 | 0.78 | 0.82 | 0.72 | 0.77 | Â | Â | Â | -30.1% | 2.6% |

| At&T Inc. | T | 0.60 | 0.57 | 0.72 | 0.72 | 0.77 | 0.64 | 0.69 | 0.69 | 0.79 | 0.75 | 0.75 | 0.76 | Â | Â | -29.7% | 3.6% |

| Wal Mart Stores | WMT | 0.44 | 0.51 | 0.57 | 0.57 | 0.75 | 0.61 | 0.72 | 0.66 | 0.71 | 0.61 | 0.64 | 0.73 | 0.66 | Â | -34.4% | 2.7% |

| Exxon Mobil Cp | XOM | 0.49 | 0.56 | 0.71 | 0.72 | 0.81 | 0.64 | 0.71 | 0.72 | 0.78 | 0.76 | 0.76 | 0.78 | 0.81 | 0.67 | 1.9% | 4.3% |

| Portfolio | -44.6% | 3.1% |

Historically, the same portfolio has exhibited correlations between the various components which have been considerably lower. In fact, over the past twenty years (February 2nd, 1989 to Jan 30th, 2009), correlations have averaged 0.32, approximately half the correlation we have seen recently. The standard deviation of the daily returns was only 1.1%

|

Â

|

| BAC | GE | IBM | INTC | JNJ | KO | MCD | MMM | MRK | MSFT | PFE | PG | T | WMT | Return | StdDev |

| Bk Of America Cp | BAC | Â | Â | Â | Â | Â | Â | Â | Â | Â | Â | Â | Â | Â | Â | 3.2% | 2.5% |

| Gen Electric Co | GE | 0.49 | Â | Â | Â | Â | Â | Â | Â | Â | Â | Â | Â | Â | Â | 8.4% | 1.8% |

| Intl Business Mac | IBM | 0.31 | 0.41 | Â | Â | Â | Â | Â | Â | Â | Â | Â | Â | Â | Â | 7.3% | 1.9% |

| Intel Corporation | INTC | 0.31 | 0.40 | 0.45 | Â | Â | Â | Â | Â | Â | Â | Â | Â | Â | Â | 15.4% | 2.7% |

| Johnson And Johns | JNJ | 0.27 | 0.39 | 0.23 | 0.22 | Â | Â | Â | Â | Â | Â | Â | Â | Â | Â | 14.5% | 1.5% |

| Coca Cola Co The | KO | 0.28 | 0.38 | 0.21 | 0.22 | 0.41 | Â | Â | Â | Â | Â | Â | Â | Â | Â | 12.4% | 1.6% |

| Mcdonalds Cp | MCD | 0.27 | 0.36 | 0.24 | 0.22 | 0.30 | 0.34 | Â | Â | Â | Â | Â | Â | Â | Â | 12.9% | 1.7% |

| 3 M Company | MMM | 0.35 | 0.45 | 0.28 | 0.29 | 0.31 | 0.34 | 0.28 | Â | Â | Â | Â | Â | Â | Â | 9.1% | 1.5% |

| Merck Co Inc | MRK | 0.27 | 0.36 | 0.23 | 0.22 | 0.51 | 0.35 | 0.26 | 0.28 | Â | Â | Â | Â | Â | Â | 8.2% | 1.9% |

| Microsoft Corpora | MSFT | 0.31 | 0.41 | 0.41 | 0.55 | 0.28 | 0.27 | 0.23 | 0.26 | 0.26 | Â | Â | Â | Â | Â | 21.5% | 2.3% |

| Pfizer Inc | PFE | 0.30 | 0.40 | 0.25 | 0.23 | 0.52 | 0.35 | 0.27 | 0.29 | 0.54 | 0.29 | Â | Â | Â | Â | 12.0% | 1.8% |

| Procter Gamble | PG | 0.27 | 0.37 | 0.19 | 0.20 | 0.41 | 0.43 | 0.33 | 0.34 | 0.35 | 0.21 | 0.36 | Â | Â | Â | 14.3% | 1.6% |

| At&T Inc. | T | 0.32 | 0.37 | 0.26 | 0.25 | 0.32 | 0.32 | 0.27 | 0.29 | 0.29 | 0.28 | 0.29 | 0.30 | Â | Â | 8.4% | 1.8% |

| Wal Mart Stores | WMT | 0.32 | 0.45 | 0.29 | 0.30 | 0.34 | 0.36 | 0.32 | 0.35 | 0.31 | 0.33 | 0.33 | 0.34 | 0.32 | Â | 13.8% | 1.8% |

| Exxon Mobil Cp | XOM | 0.29 | 0.37 | 0.26 | 0.24 | 0.33 | 0.34 | 0.25 | 0.37 | 0.31 | 0.28 | 0.32 | 0.27 | 0.35 | 0.29 | 13.5% | 1.5% |

| Portfolio | 13.2% | 1.1% |

All these results were created using the tools at AssetCorrelation.com

ABOUT

"What of the dreams that never die?"